Blockchain Facts: What Is It, How It Works, and How It Can Be Used

Blockchain definition:

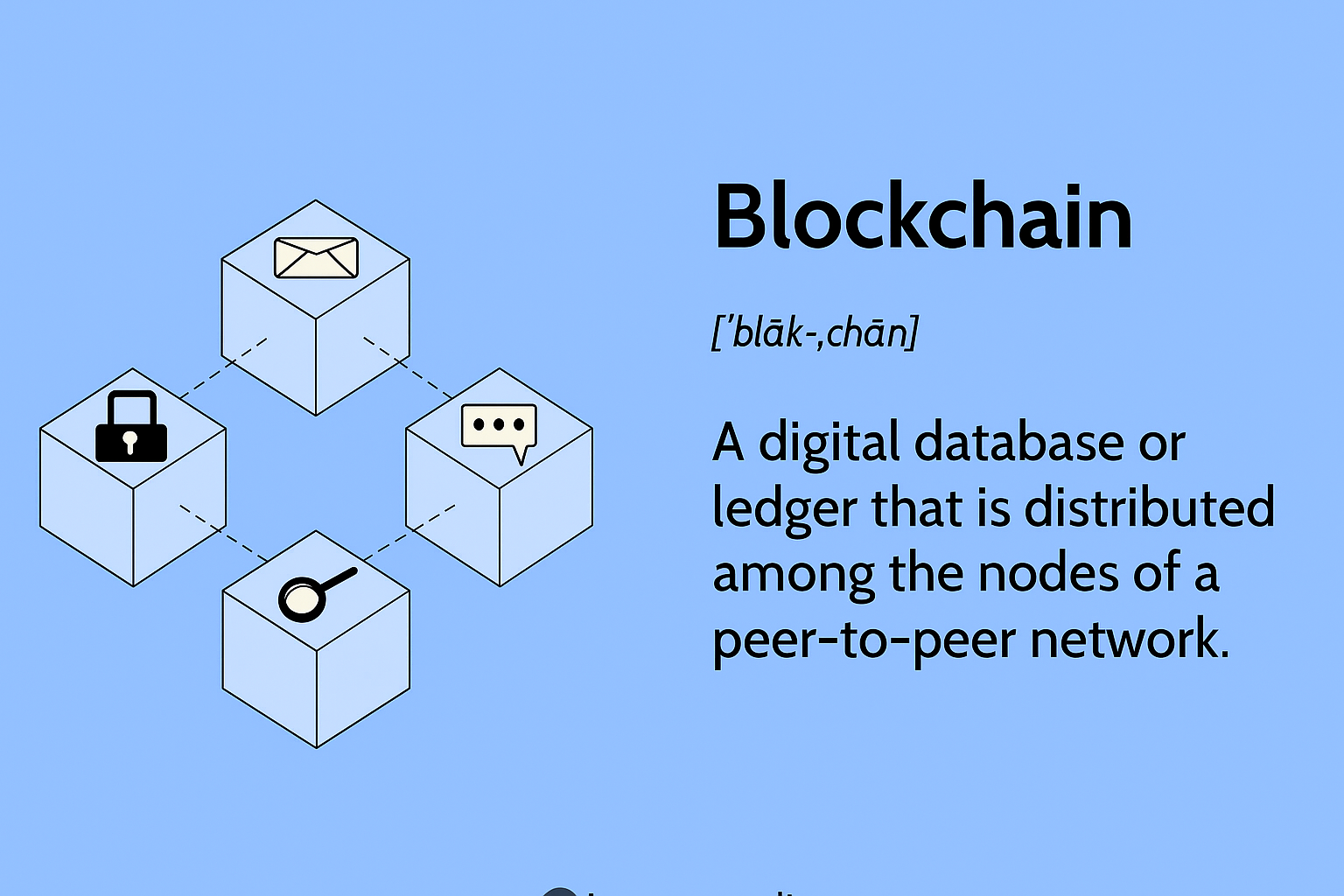

Blockchain refers to a decentralized digital ledger technology that allows information to be recorded securely across multiple computers. It ensures transparency, cannot be altered once recorded, and resists unauthorized changes. Each “block” carries specific data, and these blocks are connected in order to form a continuous “chain.”

What Is a Blockchain?

Blockchain is a decentralized digital ledger that runs on a computer network. Although blockchain technology is most frequently linked to cryptocurrencies like Bitcoin, its uses are far more extensive. It guarantees that data in a variety of industries stays safe, transparent, and unalterable.

Because each data block is permanent once added, blockchain eliminates the need to rely heavily on third-party verification—reducing costs and minimizing human errors. The trust lies in the system itself, not in intermediaries.

Since Bitcoin launched in 2009, blockchain has rapidly evolved. It now powers a range of innovations including decentralized finance (DeFi), smart contracts, and non-fungible tokens (NFTs). This growth highlights blockchain’s potential to revolutionize how we store, share, and secure information in a digital world.

Key Takeaways

Blockchain is a type of distributed database that sets itself apart from traditional databases by the way it organizes and secures data—information is grouped into blocks, and each block is cryptographically linked to the next.

While a blockchain can store various types of information, its most widely recognized application is recording financial transactions.

In the case of Bitcoin, the blockchain operates in a decentralized manner, meaning no single entity has authority over the data; instead, all participants collectively maintain and govern the system.

One of the key features of decentralized blockchain networks is immutability—once data is added, it cannot be changed or removed. For Bitcoin, this ensures that every transaction is permanently logged and transparently visible to anyone.

How Does a Blockchain Work?

You already have a basic understanding of how a blockchain operates if you have ever worked with databases or spreadsheets. However, a blockchain organizes and secures data in a very different—and far more powerful—way than traditional databases, which store data in tables or fields.

A blockchain is fundamentally a kind of digital ledger. However, it is dispersed throughout a network of computers rather than being kept on a single server. This indicates that each participant (referred to as a node) has a copy of the data, and all copies must concur for any information to be deemed legitimate.

What makes blockchain unique is the way it records and links data. Instead of simple rows in a table, data is bundled into “blocks.” Each block contains a set of data, and once it’s full, it’s sealed using a cryptographic process. The block’s information is run through a hash function—a complex algorithm that turns data into a unique string of numbers and letters called a hash. This hash is then used to link the block to the next one, forming a continuous, secure chain—hence the name blockchain.

How Blockchain Transactions Work

Every blockchain handles transactions in its own way, but the general idea is similar across platforms. Take Bitcoin’s blockchain for example. When you send Bitcoin using your crypto wallet (which connects you to the blockchain), your transaction begins a series of steps.

First, the transaction goes to a memory pool, where it’s held temporarily until a miner selects it for processing. When enough transactions are collected to fill a block (in Bitcoin’s case, up to 4MB of data), the block is sealed, and the mining process starts.

Each node in the network can propose its own version of the block using different transactions. They all compete to find a cryptographic solution, using a special variable called a nonce (short for “number used once”).

The Role of Mining and Proof-of-Work

The nonce is part of the block’s header and can be adjusted with each attempt to find the correct hash. If the generated hash doesn’t meet the required difficulty level, miners increment the nonce and try again. This can happen billions of times per second. Once they exhaust all possible nonce values, they begin changing another value known as the extra nonce.

This process of trial and error continues until a valid hash is discovered. This is what’s known as proof-of-work—a computational effort that proves a miner did the work to find a valid hash. It’s this rigorous process that makes the Bitcoin network secure but also highly energy-consuming.

What Happens After a Block Is Mined?

Once a valid block is mined, the transaction within it is considered complete. However, for added security, the network doesn’t fully confirm the block until five more blocks have been added after it. Since Bitcoin adds one block roughly every 10 minutes, a full confirmation takes around one hour.

Not All Blockchains Work the Same Way

It’s important to note that not every blockchain relies on proof-of-work. For instance, the Ethereum blockchain uses a system called proof-of-stake. In this model, a validator is randomly selected from those who have locked (or “staked”) their Ether. That validator then confirms the block, and the network agrees on its validity. This method is significantly faster and consumes much less energy compared to Bitcoin’s system.

Blockchain Decentralization

Blockchain is a technology that distributes data across multiple network nodes—these are computers or devices that run blockchain software—spread out in different locations. This setup not only ensures data accuracy but also adds a layer of redundancy. For instance, if someone attempts to change a piece of data on one node, the other nodes can detect the inconsistency by comparing block hashes and block the change. This means no single computer can tamper with the information stored on the blockchain.

Blockchain guarantees that data, such as transaction records, cannot be changed after it has been added because of its decentralized structure and cryptographic validation. These documents are irrevocable. Although many people think of blockchain in relation to financial transactions, private blockchains can also store other kinds of data, like government-issued identification documents, digital contracts, or stock data from a company. Usually, these documents are not directly stored on the blockchain. Rather, hashing algorithms transform them into distinct cryptographic codes, which are then stored on the blockchain as safe tokens.

Blockchain Transparency

Due to the decentralized structure of the Blockchain, especially in Bitcoin’s case, every transaction is fully transparent. Anyone can access and view these transactions by either downloading the blockchain or using blockchain explorers, which display real-time transaction activity. Each node in the network stores its own updated copy of the blockchain, reflecting every newly confirmed block. This makes it possible to trace a Bitcoin wherever it moves.

Take past crypto exchange hacks, for instance—large sums of cryptocurrency have been stolen. Even though the hackers may have remained anonymous aside from their wallet addresses, the stolen funds can still be tracked. That’s because all wallet addresses and transactions are permanently recorded on the blockchain.

Most records stored on the Bitcoin blockchain—and other blockchains as well—are encrypted. Only the person who controls a specific address can reveal their identity. This unique feature allows blockchain users to maintain anonymity while ensuring full transparency.

Is Blockchain Secure ?

Blockchain is a revolutionary technology that provides decentralized security and trust through a unique combination of structure and cryptography. One key aspect of blockchain is that new data blocks are added in a linear, chronological order—each one following the last. Once a block is added, it becomes nearly impossible to change any data within it without altering every block that comes after.

This is because each block in a blockchain contains a cryptographic hash of the previous block. If someone tries to tamper with a block’s data, its hash changes, which causes a mismatch in all the following blocks. Since the entire network must agree on the blockchain’s state, any inconsistency is automatically flagged and rejected by most nodes.

But is Blockchain truly unbreakable?

Not entirely. While blockchain networks are designed to be secure, they’re not invincible. Their strength depends heavily on the quality of their code and the scale of their network. Smaller blockchain networks are more vulnerable, especially to what’s known as a 51% attack. In this scenario, if a single entity gains control of over half the network’s computing power, they could potentially manipulate the blockchain.

On massive networks like Bitcoin, this kind of attack is practically impossible. By September 2024, the Bitcoin network was processing hashes at a staggering rate of over 640 exahashes per second—an astronomical number that makes any tampering attempt obsolete before it even starts.

Ethereum, another major blockchain platform, is also highly secure due to its proof-of-stake system. As of September 2024, more than 33.8 million ETH had been staked by over a million validators. To compromise the Ethereum blockchain, an attacker would need to own and control over 17 million ETH and be repeatedly chosen to validate blocks—an extremely unlikely scenario.

In short, blockchain combines cryptography, decentralization, and community consensus to build a secure, trustworthy, and transparent system that’s incredibly difficult to compromise.

Bitcoin vs. Blockchain

Researchers Stuart Haber and W. Scott Stornetta first proposed the idea of blockchain in 1991. Their objective was to develop a safe system that would prevent tampering or alteration of document timestamps. But it wasn’t until January 2009, almost 20 years later, that the world witnessed the first practical application of blockchain technology with the introduction of Bitcoin.

Bitcoin: Blockchain in Action

Bitcoin’s foundation is built entirely on blockchain technology. In the original whitepaper, Bitcoin’s mysterious creator—known only by the pseudonym Satoshi Nakamoto—described it as a “peer-to-peer electronic cash system” that operates without the need for a central authority or third party. What makes Bitcoin revolutionary is how it uses blockchain to maintain a public and transparent ledger of all transactions between users.

Blockchain Beyond Cryptocurrency

But blockchain is not just about digital money. Its power lies in its ability to record any type of data in a permanent, tamper-proof way. These records can include anything from financial transactions and property deeds to election votes, supply chain data, identity documents, and more.

Today, thousands of global projects are exploring how to harness blockchain for broader societal benefits. One promising use case is secure digital voting. By using blockchain, the voting process could become more transparent and resistant to fraud.

A New Era of Trust and Transparency

Consider a voting system in which every citizen is given a single cryptocurrency token. Voters would just send their token to the blockchain wallet address of the candidate they support, which would be unique for each candidate. This system would guarantee total transparency and accuracy because all transactions are documented on the blockchain, doing away with the need for manual vote counting and significantly lowering the possibility of election fraud.

In the end, blockchain technology is revolutionizing information security, sharing, and storage while fostering new levels of innovation and trust in a wide range of sectors.

Blockchain vs. Banks Blockchain

Blockchain technology has been hailed as a disruptive force in the financial industry, particularly in relation to banking and payment functions. Decentralized blockchains and banks, however, are very different.

Let’s compare the banking system to the blockchain implementation of Bitcoin to see how a bank and blockchain are different.

How Are Blockchains Used?

Most people instantly think of Bitcoin when they think of blockchain. Although Bitcoin was the original example of blockchain technology, its uses are not limited to cryptocurrencies. Fundamentally, a blockchain is a safe digital ledger that stores information in blocks, which makes it perfect for storing data other than financial transactions.

Companies like Walmart, Pfizer, AIG, Siemens, and Unilever are currently investigating blockchain technology in an effort to increase traceability and transparency. For example, IBM created the Food Trust blockchain to track food products as they travel from farms to stores.

Why is this important? Food safety has long been a concern, with outbreaks of E. coli, listeria, and salmonella threatening public health. Traditionally, tracing the source of contamination could take weeks. With blockchain, companies can track every point in a product’s supply chain—from origin to delivery. This rapid visibility helps identify and isolate problems more efficiently, potentially saving lives. And that’s just one example of blockchain’s practical use—there are many others being tested today.

Blockchain in Banking and Finance

Among all sectors, the financial industry stands to benefit the most from adopting blockchain. Traditional banks operate during limited hours and are closed on weekends. So, if you deposit a check on a Friday evening, you might not see the funds until Monday.

Even during business hours, verifying a transaction might take days due to the volume of processing. But blockchain doesn’t sleep. Once integrated into banking systems, blockchain could allow transactions to be completed in minutes—regardless of the day or time.

It also enables faster, safer fund transfers between banks. For institutions moving large sums of money, even minor delays can be costly. Blockchain significantly shortens the settlement time, especially in stock trading, where clearing can take up to three days. This delay ties up funds and assets unnecessarily—something blockchain could solve.

Cryptocurrency and Cross-Border Payments

Blockchain is the foundation of digital currencies like Bitcoin. But its impact extends to cross-border transactions as well. Instead of dealing with currency conversions, regulations, or unreliable banking systems, blockchain allows for direct, decentralized transfers. This makes international payments faster, cheaper, and more secure.

Blockchain in Healthcare

Healthcare is another sector being revolutionized by blockchain. Medical records are sensitive and must be kept secure and private. By recording these documents on a blockchain, healthcare providers can ensure that patient information is tamper-proof and only accessible by authorized users.

Every time a medical record is created or updated, it can be timestamped and stored securely. Patients gain confidence that their data hasn’t been altered, and providers can access an accurate history when needed.

Transforming Property Records

Anyone who has dealt with property deeds knows how inefficient the process can be. Typically, you must physically submit documents to a local office, where they’re manually entered into a public record. Errors and disputes are common—and fixing them can take weeks.

Blockchain offers a smarter solution. Property records can be digitized, stored, and verified on the blockchain, making them accurate and permanent. This not only reduces paperwork but also eliminates human error.

In areas with no formal record-keeping systems—especially war zones or underdeveloped regions—blockchain can create a transparent history of land ownership, helping communities prove property rights where governments cannot.

Smart Contracts: Automating Agreements

Smart contracts are programs built on the blockchain that automatically execute when certain conditions are met. This allows for secure, self-enforcing agreements between parties—no lawyers or intermediaries needed.

From real estate deals to freelance work, smart contracts can simplify and automate transactions, reducing the chances of fraud or misunderstanding.

Boosting Supply Chain Transparency

Blockchain is changing how companies track the origin of products and materials. By logging each step in the supply chain, businesses can verify where an item came from and how it was handled.

This is particularly useful for verifying claims like “Organic” or “Fair Trade.” IBM’s Food Trust platform, for instance, helps ensure food safety and authenticity from farm to table—a trend increasingly adopted across the industry, as reported by Forbes.

Blockchain in Voting Systems

Another powerful application of blockchain is in digital voting. In 2018, West Virginia tested blockchain-based voting during the U.S. midterm elections, demonstrating its potential to eliminate fraud and increase voter participation.

With blockchain, votes are securely recorded, transparent, and immutable. This reduces the need for manual counting, cuts down on election staff, and delivers results almost instantly. Such a system could restore trust in democratic processes while saving time and resources.

Pros and Cons of Blockchain

Blockchain’s potential as a decentralized method of record-keeping is nearly limitless, despite its complexity. Blockchain technology may find uses beyond those listed above, ranging from increased security and user privacy to reduced processing costs and fewer mistakes. However, there are some drawbacks as well.

Improved accuracy by removing human involvement in verification

Cost reductions by eliminating third-party verification

Decentralization makes it harder to tamper with

Transactions are secure, private, and efficient

Transparent technology

Provides a banking alternative and a way to secure personal information for citizens of countries with unstable or underdeveloped governments

Significant technology cost associated with some blockchains

Low number of transactions per second

History of use in illicit activities, such as on the dark web

Regulation varies by jurisdiction and remains uncertain

Data storage limitations

Benefits of Blockchains

The Power and Potential of Blockchain Technology

1. Enhanced Accuracy Through Distributed Validation

Blockchain ensures high levels of accuracy by removing human involvement from the transaction verification process. Instead of relying on a single entity, transactions are validated by thousands of nodes (computers) on the blockchain network. This widespread verification system minimizes the risk of human error. Even if one node makes a mistake, it doesn’t affect the entire system—since the network won’t accept an incorrect version of the blockchain.

2. Lower Operational Costs

Traditionally, verifying transactions requires intermediaries like banks or notaries, which adds extra fees. Blockchain removes the need for these third-party verifications, drastically reducing costs. For instance, credit card transactions involve bank processing fees. Blockchain-based currencies like Bitcoin operate without a central authority, offering significantly lower transaction fees for businesses and individuals alike.

3. Decentralized Data Storage

Unlike centralized databases, blockchain doesn’t store data in one location. Instead, it distributes identical copies of the ledger across a vast network of computers. Every time a new block is added, each system in the network updates its ledger automatically. This decentralized design makes blockchain much harder to hack or corrupt since no single point of failure exists.

4. Faster and More Efficient Transactions

Conventional banking systems often take several days to process and settle transactions—especially over weekends or holidays. Blockchain operates continuously, 24/7/365, enabling much quicker transaction settlements. On certain blockchain platforms, payments can be processed and secured within minutes. This speed is especially beneficial for international transfers, where delays due to time zones and intermediaries are common.

5. Privacy Without Total Anonymity

Blockchain networks often function as public ledgers accessible to anyone online. While transaction data is visible, user identities remain protected. Instead of showing names, blockchain uses cryptographic addresses. This means transactions are pseudonymous—not fully anonymous—but still offer a layer of privacy unless specific identities are revealed through external means.

6. Strong Security Protocols

Once a transaction is recorded on the blockchain, the entire network must validate its authenticity. After approval, it becomes part of a permanent block. Every block contains its own unique code (hash) and references the hash of the previous block. This cryptographic linking ensures that blocks are virtually unchangeable once confirmed, safeguarding the data against tampering.

7. Transparent and Open Source

Many blockchain systems, such as Bitcoin, are open-source. This means anyone can inspect the code, which promotes trust and allows independent auditing. Developers across the globe can suggest improvements. If a majority of network participants agree with an update, it can be implemented. This democratic structure ensures the blockchain evolves collectively, not under the control of a single authority.

However, private or permissioned blockchains operate differently. These systems may limit access to only approved users, allowing organizations to control data visibility for confidentiality or compliance purposes. In the future, publicly traded companies might even be required to use blockchain for financial transparency, ensuring accurate and tamper-proof reporting.

8. Financial Access for the Unbanked

One of the most transformative aspects of blockchain and cryptocurrencies is their ability to provide financial tools to people without access to traditional banking. According to the World Bank, over 1.4 billion adults lack bank accounts—many of whom live in underdeveloped nations where cash is the only option.

These individuals often store physical money in unsafe locations, putting them at risk of theft or loss. Blockchain and crypto can change that by offering a secure, digital way to store and transfer value. Although not entirely theft-proof, digital assets are significantly harder to steal than cash, giving vulnerable populations better financial protection.

Drawbacks of Blockchains

Blockchain is by no means a free solution, even though it promises to reduce transaction fees and offer more secure digital interactions. For instance, the proof-of-work (PoW) mechanism of Bitcoin requires a significant amount of processing power in order to validate transactions. In actuality, the combined energy consumption of all the devices that support the Bitcoin network is higher than Pakistan’s yearly energy consumption.

Nevertheless, more environmentally friendly methods are starting to appear. To lessen blockchain’s environmental impact, some mining companies are now utilizing renewable energy sources, such as wind turbines, solar-powered farms, and even excess natural gas from hydraulic fracturing.

Blockchain’s Struggles with Speed and Efficiency

The decentralized nature of blockchain brings with it certain limitations—most notably speed. Bitcoin is often cited as a case study in blockchain inefficiency. Due to its PoW system, adding a new block takes about 10 minutes, which translates to roughly seven transactions per second (TPS). In contrast, legacy systems like Visa can handle up to 65,000 TPS.

Other blockchain platforms, like Ethereum, offer improvements but still face performance bottlenecks due to the underlying structure. Fortunately, several blockchain projects are now being developed that claim they can handle tens of thousands of TPS. Ethereum’s ongoing upgrades—such as data sampling, BLOBs (binary large objects), and rollups—aim to reduce congestion, speed up transactions, lower fees, and boost network capacity.

Another challenge lies in the limited data capacity per block. This long-standing issue continues to hinder the scalability of blockchain systems.

The Dark Side: Blockchain and Illicit Use

User privacy, one of blockchain’s most lauded features, can also be its most contentious. Because of the anonymity it offers, it has been used to support unlawful activity. The Silk Road, an underground dark web marketplace that was used for money laundering and drug sales from 2011 until its closure by the FBI in 2013, is a well-known example.

Users can conduct anonymous transactions that are difficult to track down by using programs like the Tor Browser and cryptocurrencies like Bitcoin. This is in stark contrast to U.S. financial regulations, which require service providers to check for terrorist affiliations and confirm identities when opening accounts for customers.

✅ Note: In 2023, only 0.34% of cryptocurrency transactions were linked to illicit activities.

So, while blockchain can empower financial inclusion for people without bank access, it also opens doors for criminal use. Still, many argue that its benefits outweigh the risks, especially when the majority of illegal dealings continue to happen using untraceable physical cash.

Public Trust and Blockchain Skepticism

Despite all the innovation, public opinion on blockchain and cryptocurrencies remains mixed. Past incidents like the collapse of Mt. Gox in 2014 and FTX in 2022, along with ongoing scams and volatility, have shaken user confidence. As of 2024, a recent survey found that 44% of Americans said they would never invest in cryptocurrency.

This hesitancy is also fueled by a broader discomfort with rapid technological change and distrust in the promise of a fully decentralized financial system.

Blockchain Regulation: A Growing Conversation

The regulatory landscape for blockchain and cryptocurrencies is still taking shape. Governments around the world are beginning to tighten restrictions on crypto-related products, though there are currently no direct regulations targeting blockchain development itself.

As the technology evolves, regulatory frameworks will need to balance innovation with consumer protection, without stifling blockchain’s transformative potential.

Storage Challenges in a Blockchain World

Blockchain isn’t just about transactions; it’s also about data storage. As blockchains grow in size, the need for efficient and scalable storage becomes more urgent. Since many blockchains require nodes to store the entire transaction history, the storage demands increase over time.

For instance, by September 15th, 2024, the Bitcoin blockchain exceeded 600 GB in size—just for Bitcoin transactions. While this might seem small compared to today’s data centers, the proliferation of blockchain networks across industries could massively inflate storage needs.

This means more advanced storage solutions must be developed, or users will need to constantly upgrade hardware—potentially leading to significant costs in both space and infrastructure.

How Are Blockchains Used?

❓ 1. What exactly is a blockchain?

A blockchain is a decentralized digital ledger composed of blocks containing data. These blocks are cryptographically linked in a chronological chain, making tampering nearly impossible.

❓ 2. How does a blockchain work?

Each block holds a set of transactions, which are hashed and connected to the previous block’s hash. Through consensus mechanisms like Proof‑of‑Work (e.g., Bitcoin) or Proof‑of‑Stake (e.g., Ethereum), network nodes validate and add new blocks across the distributed ledger .

❓ 3. Is blockchain secure?

Yes—it’s secure because altering a block changes its hash. Since each block references the previous one, tampering breaks the chain. To overwrite it, attackers would need to control over 50% of the network’s computing power, which is virtually impossible on large networks.

❓ 4. What are the main benefits of blockchain?

Blockchain offers:

Transparency: anyone can trace transactions.

Immutability: records can’t be changed once added.

Decentralization: no central authority controls the network.

Efficiency & cost savings: transactions can be faster and cheaper, with lower reliance on intermediaries.

❓ 5. What are the drawbacks of blockchain?

Major downsides include:

High costs: especially energy usage in Proof‑of‑Work systems.

Scalability issues: transaction throughput is low compared to traditional systems.

Regulatory uncertainty and varying privacy rules.

Storage demand: blockchain sizes grow over time, requiring increasing storage capacity.

The Bottom Line

Blockchain is a decentralized digital ledger technology that eliminates the need for middlemen and makes recordkeeping safe, transparent, and impenetrable. Although it was initially created for cryptocurrencies like Bitcoin, its uses today span sectors like supply chain management, healthcare, and finance. Blockchain technology has the potential to revolutionize data storage, sharing, and verification in a wide range of industries as it develops.

1 thought on “Blockchain Facts: What Is It, How It Works,different types, and How It Can Be Used”