For a variety of purposes, such as debt consolidation, home improvement, or medical costs, a personal loan provides flexibility. They are a wise choice because their interest rates are typically lower than those of credit cards, particularly for borrowers without assets to pledge as security.

However, if your credit score is low, personal loans may be more expensive than other options like home equity loans. Before applying, carefully consider the benefits and drawbacks of a personal loan to see if it’s right for you.

KEY:-

1. Personal loans offer flexible usage and can be utilized for nearly any financial need.

2. As per an Investopedia survey, debt consolidation remains the primary reason borrowers choose personal loans.

3. Unlike auto or home loans, personal loans typically require no collateral.

4. While cheaper than credit cards and some loan types, personal loans may still carry higher costs than others.

How Personal Loans Work

Generally speaking, a personal loan is an unsecured form of financing, which means you can borrow money without having to pledge collateral like a house or car. Lenders frequently charge higher interest rates on unsecured loans than on secured loans because they are taking on greater risk. Usually, variables like your debt-to-income ratio and credit score determine the precise rate you get.

Secured personal loans, in which you pledge assets like a car, savings account, or other property as collateral, are also provided by certain financial institutions. These loans frequently have marginally lower interest rates than unsecured ones and might be simpler to qualify for. But, as with any secured loan, if you don’t make your payments, you could lose the asset you pledged as security.

Your credit score may suffer and your future borrowing options may be limited if you miss payments on an unsecured personal loan. Your payment history is the most important factor, accounting for 35% of your total credit score, according to FICO, the company that developed the most popular credit scoring model. It’s crucial to make your payments on time.

When To Consider a Personal Loan

Before deciding on a personal loan, it’s important to explore whether there are cheaper alternatives for borrowing money. Here are a few situations where taking a personal loan may be the right choice:

- You don’t have access to or can’t get approved for a low-interest credit card.

- Your current credit card limits aren’t enough to cover your borrowing needs.

- A personal loan offers you the most affordable borrowing option.

- You lack any assets or collateral to secure another type of loan.

A personal loan might also be appropriate for you if you require funds for a brief, specific purpose. The majority of personal loans are paid back over a period of 12 to 60 months. For example, if you need money now but expect a lump sum in two years, a two-year personal loan could help you get through that time.

Here are five more circumstances in which a personal loan might make sense.

1. Consolidating Credit Card Debt

A personal loan could be a wise financial decision if you have a sizable balance on one or more high-interest credit cards. As of April 2025, for example, the average interest rate on credit cards is 24.20%, whereas the average interest rate on personal loans is significantly lower at 11.66%. Over time, this difference can lower the total amount of interest paid and help you pay off your debt more quickly. Furthermore, it’s frequently easier to manage a single loan than to balance several credit card payments.

However, there are other options besides a personal loan. If you are eligible, you may also think about moving your balances to a new credit card with a lower interest rate.

Certain balance transfer deals eliminate interest charges during a promotional period lasting six months or longer.

2. Paying off Other High-Interest Debts

VAlthough they aren’t always the most expensive, personal loans can be more costly than some other forms of credit. Payday loans, for example, usually have interest rates that are much higher than those of personal loans provided by conventional banks. Additionally, if you took out a personal loan at a time when interest rates were higher, you may be able to save money by refinancing it with a new loan at the current lower rates.

However, before switching, find out if there is a prepayment penalty on your existing loan. Additionally, investigate any origination or application fees associated with the new loan, as these can occasionally mount up and cancel out any potential savings.

3. Financing a Home Improvement or Big Purchase

A personal loan could be less expensive than financing through the retailer or using your credit card if you’re planning to install a heating system, buy new appliances, or make another significant purchase.

A home equity loan or home equity line of credit, however, might have even lower rates if you have equity in your house. However, keep in mind that both of these loans are secured, which means that if you default, your house could be in jeopardy.

4. Paying for a Major Life Event

It might be less expensive to use a personal loan rather than a credit card when organizing a large event, such as a wedding, bar or bat mitzvah, or milestone anniversary celebration. One in five American couples, according to a 2021 Brides and Investopedia survey, depend on loans or investments to pay for their wedding.

Even though these occasions are very important, if excessive spending will result in long-term debt, it is advisable to think twice. Similarly, vacation loans ought to be saved for once-in-a-lifetime experiences rather than sporadic travel. You can celebrate without worrying about the future if you practice financial mindfulness.

Important If you make all of your payments on time, a personal loan can help raise your credit score. If not, your score will suffer.

5. Improving Your Credit Score

Your credit score can be raised by taking out and paying back a personal loan on schedule, particularly if you have previously missed payments on other accounts. Adding a personal loan could diversify your “credit mix” if credit card debt makes up the majority of your credit history. When properly managed, a diverse range of credit types is frequently seen by lenders and credit bureaus as an indication of sound financial practices.

But it’s dangerous and not advised to take out a loan you don’t really need in order to raise your credit score. Maintaining a low credit utilization ratio—that is, using only a small percentage of your available credit at any given time—and regularly making on-time payments on your current bills are better strategies.

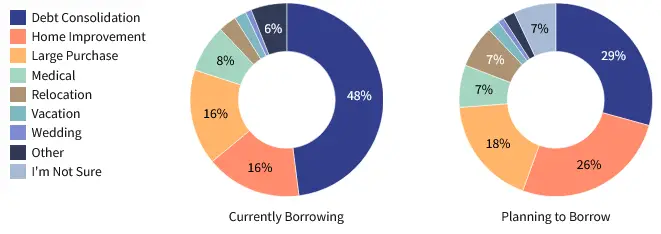

How Do People Use Personal Loans?

Key borrowing trends were identified by Investopedia’s recent nationwide survey of 962 U.S. adults who had taken out personal loans, which was conducted between August 14 and September 15, 2023. Consumer financial priorities are changing, as evidenced by the fact that debt consolidation was the most common reason for taking out personal loans, followed by home improvements and other significant expenditures.

When Shouldn’t You Use a Personal Loan?

With a few exceptions, personal loans can be used for practically anything. The following uses of personal loans are typically prohibited by lenders:

- Educational expenses, including tuition, room, board, and student loan debt

- A down payment on a house

- Business expenses

- Investing

- Gambling

Note

During the application process, lenders will ask you to specify the reason for your personal loan.

Additionally, avoid using personal loans to cover daily expenses as this could lead to a debt cycle. Instead, use your income to pay for regular expenses to avoid accruing debt.

FAQs

What Can I Use a Personal Loan For?

You can use a personal loan for nearly any purpose—such as covering a big purchase, making home upgrades, consolidating high-interest debt, or handling emergency costs. However, most lenders don’t permit using personal loans for college tuition, home down payments, or business-related expenses.

What Do I Need to Take Out a Personal Loan?

When applying for a personal loan, each lender has different requirements. You won’t require any collateral, though, because there are many unsecured personal loans available.

The Bottom Line

Although they can be useful in a variety of circumstances, personal loans are frequently expensive. Examine other financial options prior to applying. To determine whether a personal loan fits into your budget and overall financial objectives, use charchithedge personal loan calculator to estimate your monthly payments.